What is coming for satellite?

A view on new developments and the satellite technology horizon.

Please can somebody help to find a new term for satellite?

Most ICT technology innovations have some branding insight. For example, when Internet storage was developed it was immediately branded as "cloud". Similarly, the development in machine telemetry and SCADA was branded IoT. These solution brands create new energy, new expectations, and boost market acceptance. Well … for satellite … we still call it satellite even though everything is new and nothing is the same.

Perhaps we can get a new technology brand for satellite solutions as well? With all the new developments, we really need some new brands names as well. However, I can only provide a forward view using the known., and somewhat boring, terms

High-speed lower cost business services (geostationary satellites)

Did you know? Satellite is 40% faster than fibre. 2.99 x 108m/s. vs 2.14 x 108m/s.

Geostationary satellites are the backbone for enterprise, broadband and government communication networks. These are the networks for financial ATM connectivity, fibre back-up services and "off-grid" broadband services.

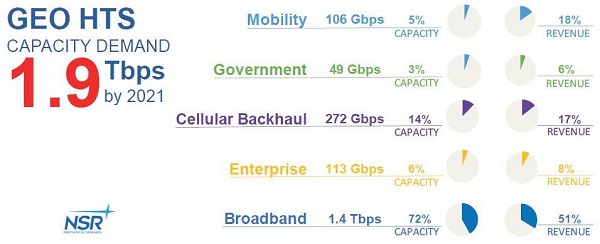

For this segment, new high-throughput digital satellite platforms were introduced 2016 / 2017 and the growth of these services is set to continue. Back in 2018, research reports by NSR predicted a capacity demand of 1.9Tbps. The current forecast is mirrored by Viasat-3 satellite launch planned for 2021 which will have 1TBbps capacity on a single satellite.

We are already seeing data rates of 100Mbps for fibre-restoration and pricing points that compare with 3G data. (refer www.twoobii.com).

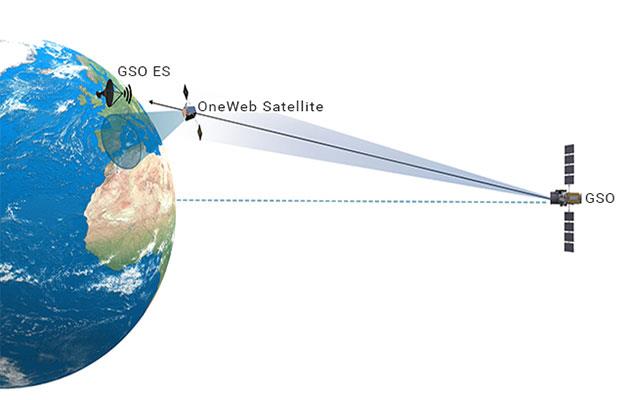

Low-Earth-Orbit (LEO) Constellations

Satellites can be in different orbital planes, and LEO constellations are 1200km above earth, creating a very different technology solution with different advantages. The OneWeb is already operating on a limited scale (with 850 satellites planned) and much was published on the expected operation of SpaceX services (6500 satellites planned). These constellations will bring solution options to the market with some expected to enter late 2020 / 2021 and initial market roll-outs in 2022.

Relative to geostationary satellites, the MEO constellations are close to earth and can benefit from shorter transmission paths, eliminating link latency concerns. This reduced the 650msec latency of GEO satellites down to less than 50msec making the alternatives to fibre networks very promising

It is expected that in 2020 the MEO operators will resolved the different deployment challenges such as regulatory compliance, ground gateway terminal and user terminal developments. Initial market evaluation systems should start entering the market in 2021.

IoT and Nanosatellites

On the other scale of the spectrum, the satellite industry is developing various short-burst data transmission solutions using nanosatellite constellations. These networks deploy small nanosatellites to provide low-volume data links to thousands of small user terminals. NSR projects strong growth with 3.7 million smallsat IoT in-service units by 2027, generating estimated $133 million in retail revenues (5% of the total M2M / I0T revenues).

The nanosatellite solutions for the African market is still under development or very early evaluation stages, and initial market solutions are only expected in 2022 or later.

The expected ARPU of this market is expected at $5 or less and a profitable deployment will require a specific large-scale specialist application. Somewhat of a business paradox.

Conclusion

Satellite solutions are changing – rapidly changing – and if you still maintain a technology view of satellite services based on a past experience you would do well to update. For 2020, the growth of high-throughput satellites is set to continue and will change the price and performance points for the broadband and enterprise markets.

Following this, the initial entries of the MEO constellations with lower latency and higher speeds are expected in 2020, with perhaps the first market deployments in 2021. These will still be very limited as the industry is developing a completely new market sectors for satellite applications.

Then the nanosatellite developments of the expected IoT industry will follow. Due to the current constellation work and user terminals development work, this is expected to be more in the 2021 / 2022 time frame.

While the satellite industry will remain a niche environment best suited to be developed by specialist service providers, the industry is undergoing major developments, is increasing in performance and lowering cost.